Industry 4.0 meets Bank 4.0

New business models in the form of real-time microtransactions can be described as an “event-driven economy” where money is transferred automatically between IoT accounts. SEB is one of the first banks to take major steps to digitize the banks' services as the industry takes similar steps towards a flexible direction.

Industry 4.0 uses technology as an enabler to further automate manufacturing and logistics. The concept "Digital Twins" often appears in the discussion, but not to forget is that today's production processes and supply chains already have "analog twins": financial and administrative functions in the form of invoicing, reconciliation, accounting, purchasing, budgeting and more.

These analog twins reflect what happens on the factory floor and in the logistics chain, often with an entire invoice period delay. The processes are slow, laborious and costly, often cut off from the core business and with a lot of manual steps along the way.

SEB as a partner in Smarta Fabriker is taking major steps to digitize and design banking services that can keep pace with Industry 4.0 - Bank 4.0. The principle is simple: to take the current range of products and services, digitize them, and then inject them into the companies' own infrastructure. In practice, the bank's products are thus moved from the bank to the conveyor belt, the truck or the robot cell.

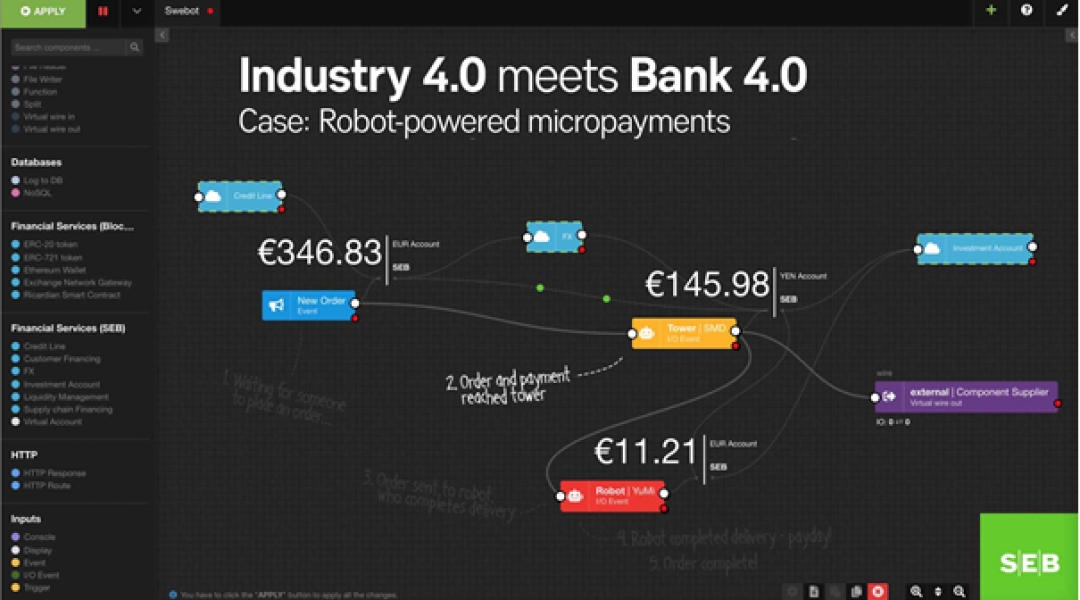

An example that SEB has developed is microtransactions between IoT accounts (pictured below). By adding the entire account structure to the IoT warehouse, an effect is obtained that can almost be described as an “event-controlled economy”. Money is transferred automatically between the stations that perform work for each other, and all microtransactions take place in real time.

The picture shows how a customer transfers money to the manufacturer, who then transfers money to a material façade at the workstation, which in turn transfers money to the AGV that fills the material façade. The AGV, in turn, transfers money to an incoming warehouse in the factory, which, when a delivery arrives, makes a microtransaction to the subcontractor. And so on.

In addition to a clarity that can quickly tell where capital is tied up, a number of new possibilities open up; here we can let sensor data such as temperature, time, kilopascal (kPa) rotations per minute or prevailing electricity price form the backbone of the business model, and with a simple code line combine and translate these data points into Swedish currency.

One such business model would be that the company does not own the AGV but instead buys the Internal Transport service in the factory and pays (in real time) per meter of distance transported. A product can easily be rented out and charged for the effect it provides. With the right sensors, the product's cost (electricity consumption and wear) can be the basis for payment.

Then the step is easy to supplement with more financial services to manage risk and reason: linking a credit to an account is done with a drag-and-drop. The same applies to automatic switching between different currencies, or VISA and MasterCard services.

Tags

This article is tagged with these tags. Click a tag to see all the articles with this tag.